How HDB Upgraders Avoid ABSD in 2026: Sell-First vs Decoupling

30 Jun 2026 · 7 min read

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Estate Agent Licence L3008899K) · Updated 30 June 2026

“Data-driven property advice. Straight talk, no hype.”

If you are moving from an HDB flat to a condominium in 2026, one worry tends to dominate: will I be hit with Additional Buyer's Stamp Duty, and how do I avoid it. For most upgraders the answer is simpler than the forums make it sound. The part that trips people up is timing and cashflow. Here are the two routes that actually work, the decoupling question everyone asks, and how to choose the right one for your situation.

Why upgrading from HDB to condo got harder in 2026

Three rules decide how much an upgrade really costs you.

The first is ABSD. A Singapore Citizen pays 0% on a first residential property but 20% on a second, according to IRAS. On a $2 million condo that 20% is $400,000, so getting the sequence right is the difference between a clean buy and a very expensive one.

The second is your loan. If you still own your HDB flat at the moment you exercise the condo's Option to Purchase, the bank treats the new home loan as a second-property loan, which caps it at about 45% of the price rather than 75%. That pulls a large amount of cash and CPF forward.

The third is affordability. Your total monthly debt is capped at 55% of gross income under the Total Debt Servicing Ratio, and banks stress-test the loan at a 4% interest floor, so your real borrowing power is tighter than today's headline rates suggest. For the full rate detail, see our complete ABSD 2026 guide.

The two routes that actually work

For an HDB upgrader the genuine choice is between selling first and buying first with a refund. Here is how they compare.

| Sell first | Buy first, claim remission | |

|---|---|---|

| ABSD upfront | $0 | 20% (refunded later) |

| Final ABSD | $0 | $0 after the refund |

| Loan to value | Up to 75% (first loan) | Second-loan rules until the flat is sold, then refinance |

| Main risk | Where to live during the gap | Cash to front the 20% and meet the 6-month deadline |

| Best for | Most upgraders, and anyone cashflow-tight | Buyers who found a unit they cannot risk losing |

Route 1: Sell your HDB flat first

You time the sale so that when you exercise the condo's Option to Purchase you no longer own the flat. The condo is then your first private property: 0% ABSD for a citizen couple, and the bank can lend up to 75%. The trade-off is the gap between selling and moving in, which you bridge with a short rental or by negotiating an extended completion or a stay request with your buyer. If you want the step-by-step on the sale side, read our guide on how to sell your HDB flat.

Route 2: Buy first, then claim the ABSD refund

Sometimes the right unit appears before your flat is sold. You can still buy it. Because you momentarily own two homes, IRAS treats the condo as a second property and charges 20% ABSD at purchase. If you are a married couple with at least one Singapore Citizen, you buy the condo in both your names only, and you sell and complete your HDB transfer within 6 months of the condo purchase, IRAS refunds the ABSD in full under its remission for married couples. If the condo is a new launch still under construction, the six-month clock runs from the project's Temporary Occupation Permit rather than the purchase date, which usually gives you far more time to sell. Miss the deadline or the conditions and the refund is lost, so this route needs both discipline and the cash to front a large sum for a few months.

What about decoupling?

Decoupling is where one co-owner buys out the other's share of a property, freeing that spouse to buy the next home as a first property and skip ABSD. Two things matter for upgraders.

First, you cannot decouple an HDB flat. HDB stopped allowing it on 1 April 2016, and ownership can only change in limited situations such as marriage, divorce, the death of an owner, or genuine financial hardship. So for the flat itself, decoupling is off the table.

Second, decoupling does work for private property. It is the route for an owner who already holds a condo and wants to buy a second without the 20% ABSD. The golden rule is to decouple only when the total cost, meaning the Buyer's Stamp Duty on the transferred share plus legal, valuation and refinancing fees, comes in below the ABSD you would otherwise pay. One caution: IRAS has audited and clawed back tax, with penalties, from contrived 99-to-1 and similar arrangements used purely to dodge ABSD. Keep any structure genuine and take proper legal advice.

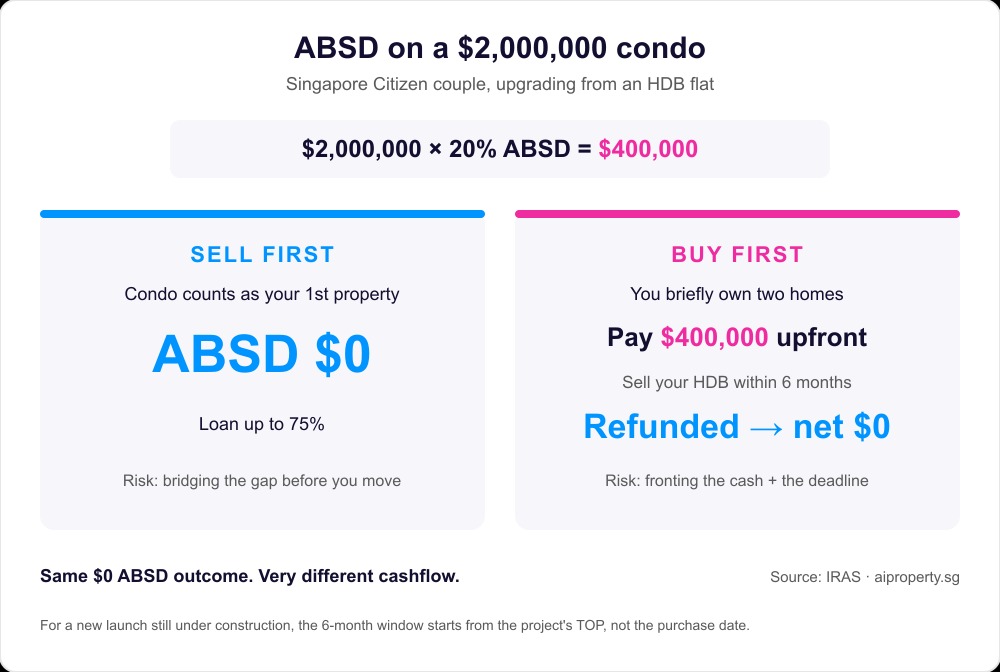

A worked example

A citizen couple is buying a $2 million condo and currently owns an HDB flat. ABSD on a second property is 20%, or $400,000. Sell the flat first and the condo becomes their first property, so ABSD is $0 and they can borrow up to 75%. Buy first instead and they pay the $400,000 upfront, then claim it back in full once the flat sale completes within 6 months. The end result on ABSD is the same. The cashflow along the way is very different.

The right sequence depends on your sale timeline, the cash and CPF you have on hand, and the unit you are chasing. I can map it for your exact situation before you commit. Message me for an upgrader plan on WhatsApp.

Which route is right for you

Most upgraders I work with sell first. It keeps ABSD at zero, unlocks the 75% loan, and lets you negotiate your condo as a cash-ready buyer rather than one juggling two mortgages. Buy first and claim remission earns its place when you have found a unit you cannot risk losing and you can comfortably fund the 20% for a few months. Either way, the deciding factors are your timeline and your cash position, not the headline price.

If you already have a project in mind, plenty of new launches sit in the typical upgrader sweet spot. Popular options include Parktown Residence in Tampines, Hougang Central Residence above the MRT in the north-east, and Lentor Gardens Residences in the Lentor estate. Whichever you are weighing, sort the ABSD sequence first so the numbers work.

Nine times out of ten, selling first is the cleaner path for upgraders. It keeps ABSD at zero, gives you the stronger loan, and you walk into the showflat as a ready buyer instead of someone hoping two timelines line up. I only steer clients to buy first when the unit is genuinely worth fronting $400,000 for a few months. Get the sequence mapped before you start viewing, not after you fall for a showflat.

By Winnie Lim, licensed CEA agent and founder of AIProperty.sg

Common questions about avoiding ABSD as an HDB upgrader

Do HDB upgraders pay ABSD on their first condo?

Not if you sell your HDB flat first. The condo then counts as your first private property, which is 0% ABSD for a Singapore Citizen couple. If you buy before selling, you pay 20% ABSD upfront and claim it back within 6 months.

Can you decouple an HDB flat to avoid ABSD?

No. HDB stopped allowing decoupling on 1 April 2016. Flat ownership can only change in limited situations such as marriage, divorce, the death of an owner, or financial hardship. Decoupling only works for private property.

How long do you have to claim the ABSD refund?

Six months. If you are a married couple with at least one Singapore Citizen and you buy the condo in both names only, you can claim a full ABSD refund when you sell and complete your HDB transfer within 6 months of the condo purchase, under IRAS remission for married couples.

How much is ABSD for a Singapore Citizen's second property?

20% as of 2026, according to IRAS. On a $2 million home that is $400,000, which is why sequencing your sale and purchase correctly matters so much.

Is selling first or buying first better?

Selling first keeps ABSD at zero and gives you a 75% loan, but you need somewhere to live during the gap. Buying first secures your unit, but you must front the 20% ABSD and meet the 6-month refund deadline. Most upgraders are better off selling first.

Plan your upgrade before you view

Thinking about making the jump from HDB to private in 2026? Message me and I will map your ABSD, timing and loan in one conversation, so you buy in the right order. WhatsApp me at +65 88772688.

This article is for general information only and should not be considered financial, legal, tax, or investment advice. Property decisions should be based on individual circumstances and independent professional advice.

About the Author

Winnie Lim is a licensed CEA real estate agent and the founder of AIProperty.sg. With a background in supply chain analytics, she brings a data-driven approach to Singapore property, and won the 2024 Million Dollar Award for consistent, client-first results.

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Licence L3008899K)

Read full bio →Continue Reading

More from Buying Guide

The Crab Bucket Effects

Crab Mentality Part 1 - Buyers (Are you one of them?)

08 Jun 2026

The New Reality of Singapore Property Buying in 2026

PSP: The Real Reason Your Parents Are Co-Signing Your Condo

27 May 2026

Drop Out ECs

Is It Worth Waiting for Drop-Out Executive Condominium (EC) Units?

20 May 2026