How to Sell Your HDB Flat in Singapore: Timeline, Costs, and the 2026 Process

15 May 2026 · 10 min read

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Estate Agent Licence L3008899K) · Updated 24 June 2026

“Data-driven property advice. Straight talk, no hype.”

How to Sell Your HDB Flat in Singapore: Timeline, Costs, and the 2026 Process

Selling an HDB flat is the most common property transaction in Singapore. Over 80% of households live in HDB, and most upgraders pass through the resale market at some point. The process is heavily structured. Most sellers underestimate how long it actually takes and how much CPF they have to refund before they see a cent.

This guide covers the 2026 process end-to-end. MOP rules, the HFE letter that now gates every sale, the 21-day OTP window, what you actually pay, CPF refunds, EIP quota traps, and the upgrader-specific ABSD risk. Numbers are accurate to May 2026 and pulled from HDB and CPF Board.

Before you list: are you eligible to sell

The Minimum Occupation Period (MOP) is five years from key collection for standard BTO flats, and from legal completion for resale flats. The clock does not start on the option date or the booking fee. It starts when you actually take possession.

Prime Location Public Housing flats (PLH) carry a 10-year MOP and additional resale restrictions, including a subsidy clawback on resale. If you bought under the PLH framework, your flat is locked up for twice as long and your sale proceeds are reduced.

You cannot sell, rent out the whole flat, buy private property, or apply for a new BTO during the MOP. Renting out individual bedrooms is allowed if owners still reside in the flat. The MOP end date sits on My HDBPage, accessible via SingPass.

If you are still inside MOP, the article you actually want is the buying or renting guide. Selling is off the table.

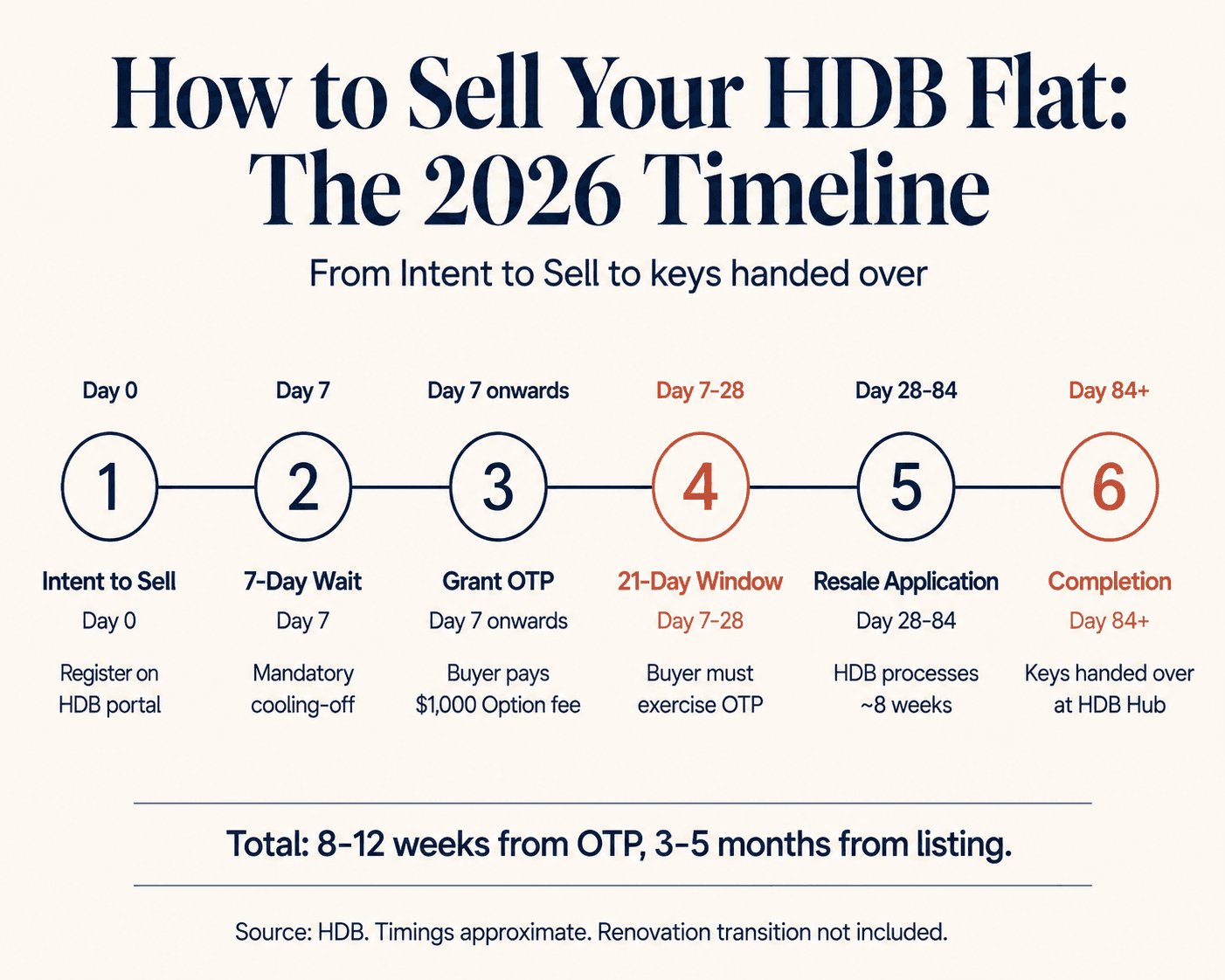

Step 1: register your Intent to Sell

The first move is to log into HDB's portal and submit the Intent to Sell. This is a free, mandatory pre-listing step that confirms your eligibility, opens up your CPF refund estimate, and produces your Resale Statement.

You must wait at least seven calendar days after the Intent to Sell is registered before you can grant the Option to Purchase (OTP) to any buyer. This is enforced by the system, no exceptions. Most sellers register the Intent to Sell as soon as they decide to list, so the seven-day window has already elapsed by the time a buyer shows up.

Step 2: price the flat and find a buyer

Pricing for HDB resale is more transparent than private. HDB publishes recent transacted prices for every block and flat type. Buyers and sellers can both pull the same data. The realistic price band for your unit is whatever the last six similar transactions in your block (or adjacent blocks) cleared at.

Two pricing levers move outside the market band. COV (Cash-Over-Valuation) is the gap between the price you and the buyer agree on and the HDB valuation. It is paid in cash by the buyer, on top of any down payment. In a strong market, COV climbs. In a soft market, it goes to zero or sellers cut the asking price. Renovation premium. A well-renovated flat with newer kitchen, bathrooms, and flooring typically commands 3 to 8% above the unrenovated comp.

For market exposure, most sellers either list themselves on the HDB Resale Portal (free) or engage an agent. Agent commission for sellers is typically 1% of sale price plus GST. The buyer pays their own agent separately, usually 1%.

Step 3: the HFE letter rule

Before you can grant any OTP, the buyer must have a valid HDB Flat Eligibility (HFE) letter. The HFE was introduced to consolidate the buyer's eligibility check, loan estimate, and grant entitlement into one document. It is valid for six months. The buyer cannot proceed without it.

Ask any prospective buyer for their HFE letter before you accept their offer. A buyer without an HFE is not a real buyer. They can apply for one online but it takes around two weeks to issue, and that two weeks is dead time you do not want during a sale window.

Step 4: grant the OTP and the 21-day window

Once a buyer is HFE-cleared and price is agreed, you grant the OTP. The Option fee can be anywhere from $1 to $1,000. Market practice in 2026 is $1,000. This fee is non-refundable to the buyer if they walk away.

From the OTP date, the buyer has 21 calendar days to exercise the option by paying the rest of the deposit (typically another $4,000, capped at $5,000 in total upfront). During this 21-day window, you cannot accept any other offers, even higher ones. If the buyer does not exercise, the OTP lapses and you keep the Option fee.

If the buyer exercises within the 21 days, both sides submit the resale application to HDB. The clock to completion starts.

Step 5: the resale application and HDB processing

The resale application is filed jointly through the HDB portal. Both parties submit. The application fee is $40 for 1- and 2-room flats, $80 for 3-room and larger.

HDB processes the application in around eight weeks. During this window, the buyer's loan documents are finalised, both sides' lawyers complete title checks, HDB issues an in-principle approval, and a completion date is set. Most sellers and buyers do not need to do anything during this stretch other than respond promptly to HDB queries (if any).

Step 6: the completion appointment

On the completion date, both parties meet at HDB Hub. The buyer pays the balance. The seller transfers possession and keys. The lawyers handle the conveyancing paperwork on the spot.

Completion is when the seller actually sees money. Until this date, you have only seen the $1,000 Option fee and the buyer's deposit (which is held in escrow). The bulk of your proceeds, less your CPF refund and any outstanding loan, lands on completion day.

The ABSD timing between selling your flat and buying private is where most upgraders lose money. Get an ABSD-timing plan for your upgrade.

What you actually pay as the seller

| Line item | Amount |

|---|---|

| HDB resale application fee | $40 to $80 |

| Conveyancing (HDB lawyer) | $800 to $1,500 |

| Conveyancing (private lawyer) | $1,800 to $3,000 |

| Agent commission (optional) | 1% of sale price plus GST |

| Existing loan early redemption fee | varies by lender, often 1.5% within lock-in |

| Property tax (annual, prorated) | depends on AV and ownership type |

A clean sale on a $600,000 4-room flat without a remaining loan and using the HDB lawyer typically nets the seller around $593,000 to $594,000 after costs, before CPF refund.

CPF refund: what really comes out

This is where most sellers get a surprise. Every cent of CPF used to buy the original flat must be refunded to your CPF Ordinary Account on sale, with accrued interest. That accrued interest builds up at 2.5% per year from the date you first withdrew the CPF. Over a 10-year hold, the accrued interest can add 25 to 30% on top of the principal.

So if you used $200,000 CPF to buy a flat 10 years ago, the refund on sale is roughly $256,000, not $200,000. That is money that goes back into your CPF (where it can be used for the next property), not into your bank account.

The cash you actually walk away with is: sale price minus outstanding loan minus CPF refund (principal plus accrued interest) minus legal fees minus agent commission.

Negative sale rule

If the math leaves you short (the sale price is less than the outstanding loan plus CPF refund), you do not have to top up the gap in cash. As long as the flat sold at fair market value (the HDB valuation or above), the CPF Board waives the shortfall. The bank loan still gets paid off in full from the proceeds first; CPF takes whatever is left.

EIP and SPR quota: the gating risk

HDB enforces an Ethnic Integration Policy (EIP) at the block and neighbourhood level. The policy caps the percentage of households of each ethnic group (Chinese, Malay, Indian and Others, also called CMIO) in any given HDB block. There is also a separate cap on Singapore Permanent Resident (SPR) households.

For sellers, the EIP limits who you can sell to. If your block has already hit the cap for your ethnic group, your buyer must come from an ethnic group that keeps the block within the quota. In practice this hurts minority sellers most often. Studies show minority-owned flats in EIP-constrained blocks frequently sell for less or stay on market longer because the eligible buyer pool is smaller.

HDB updates the quotas on the 1st of each month. Check yours before you list. If you are EIP-constrained and the flat is hard to move at fair value, HDB now has a buyback scheme for genuine cases.

The upgrader trap: ABSD on the next property

The most expensive mistake HDB sellers make is buying the next property before selling. If you commit to a $2 million private condo while still holding your HDB, you pay 20% ABSD ($400,000) on the new property at the point of purchase.

The remission rule lets you claim the $400,000 back if you sell the HDB within six months of the new condo's OTP date (or six months of TOP for new launches). Miss that window and the ABSD becomes permanent. The full breakdown is in our complete 2026 ABSD guide.

Most upgraders moving into the new launch market under S$3 million go one of three ways. Sell first, rent for 6 to 12 months, then buy. Cleanest, slowest. Buy second, then race to sell within the 6-month window. Most common, requires bridging finance. Buy in only one spouse's name (if the HDB is in both names, this fails — see the ABSD article for the full mechanic).

Bottom line

Selling an HDB flat is not complicated, but it is heavily sequenced. Eight to twelve weeks from OTP to keys, plus a few weeks of pre-OTP search and waiting. The biggest surprises sit on the financial side: the CPF refund consumes a chunk of your proceeds you may have forgotten about, and the upgrader ABSD window is unforgiving.

Three things to set up before you list. First, register the Intent to Sell so the seven-day window is already used up. Second, check the EIP quota for your block. Third, do the math on your CPF refund and accrued interest before you imagine the cash you will pocket. The number on the contract is not the number that hits your bank account.

I can walk you through pricing, the timeline, and your CPF refund so there are no surprises at completion. Talk to me on WhatsApp.

Further reading

- ABSD Singapore Explained: Rates, Remission, and the Full 2026 Breakdown. For the upgrader-side stamp duty math and the 6-month remission window.

- Buying Property in Singapore as a Foreigner: The Complete 2026 Guide. If your buyer is a PR or foreigner, the rules and timing differ.

- Browse private listings in District 9 and District 10 if you're upgrading from HDB to private, or compare District 11 listings for a quieter central option.

Sources

- HDB — Selling a Flat Overview

- HDB — Eligibility to Sell

- HDB — Minimum Occupation Period

- HDB — Ethnic Integration Policy (EIP) and SPR Quota

- CPF Board — Using CPF for Property

- IRAS — Additional Buyer's Stamp Duty (ABSD)

Common questions about selling an HDB flat

How long does it take to sell an HDB flat in Singapore?

From granting the Option to Purchase to collecting keys takes roughly eight to twelve weeks, plus a few weeks of searching and waiting beforehand. HDB processes the resale application in about eight weeks once both parties submit. The buyer has 21 days from the OTP date to exercise the option.

Do I have to refund my CPF when I sell my HDB flat?

Yes. Every dollar of CPF used to buy the flat must be returned to your CPF Ordinary Account with accrued interest at 2.5% per year. Over a ten-year hold, the accrued interest can add 25 to 30% on top of the principal. The refunded amount can fund your next property.

What is the MOP and can I sell before it ends?

The Minimum Occupation Period is five years from key collection for standard BTO flats, or ten years for Prime Location Public Housing flats. You cannot sell, rent out the whole flat, or buy private property during the MOP. The end date is shown on My HDBPage.

Will I pay ABSD if I buy a condo before selling my HDB?

Yes, you pay 20% ABSD on the new property because you briefly own two homes. You can claim it back if you sell the HDB within six months of the new purchase, or within six months of TOP for a new launch. Many upgraders use bridging finance to cover the gap.

This article is for general information only and should not be considered financial, legal, tax, or investment advice. Property decisions should be based on individual circumstances and independent professional advice.

About the Author

Winnie Lim is a licensed CEA real estate agent and the founder of AIProperty.sg. With a background in supply chain analytics, she brings a data-driven approach to Singapore property, and won the 2024 Million Dollar Award for consistent, client-first results.

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Licence L3008899K)

Read full bio →Continue Reading

More from Selling Guide

Sellers in the Bucket

Crab mentality hits sellers too. Neighbour comparisons, inflated valuations, and wait for a better market advice can cost you. Here is how to sell free of it.

08 Jun 2026

How Much Do You Really Need to Buy a Condo in Singapore? Down Payment, TDSR and Stamp Duty

How much cash and CPF you really need to buy a condo in Singapore in 2026: the 25% down payment and 5% cash rule, the TDSR loan limit, Buyer's Stamp Duty, and the full upfront cost on a $2 million example.

01 Jul 2026

How HDB Upgraders Avoid ABSD in 2026: Sell-First vs Decoupling

How Singapore HDB upgraders legally avoid or recover ABSD in 2026: the sell-first route, the buy-first 6-month remission, why you cannot decouple an HDB, and how decoupling works for private owners.

30 Jun 2026