Buying Property in Singapore as a Foreigner: The Complete 2026 Guide

15 May 2026 · 9 min read

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Estate Agent Licence L3008899K) · Updated 24 June 2026

“Data-driven property advice. Straight talk, no hype.”

Buying Property in Singapore as a Foreigner: The Complete 2026 Guide

Singapore is one of the most foreigner-friendly property markets in Asia, until you see the tax bill. A foreigner buying a $3 million condo in District 9 pays $1.92 million in stamp duty before keys change hands. That is the entry cost.

This guide covers what you can and cannot buy as a non-resident, how the FTA exemption works, who qualifies for financing, and what the actual buying timeline looks like from offer to handover. Numbers are accurate to May 2026 and pulled from IRAS, SLA, and MAS.

What foreigners can buy

The rules sit in the Residential Property Act. There are three tiers, and the differences matter.

Open to foreigners. No approval needed.

- Private condominiums and apartments (non-landed)

- Strata-titled units in approved developments

- Executive Condominiums (ECs) that are at least 10 years old and fully privatised

- Commercial property (offices, retail, industrial)

- Sentosa Cove landed homes, with strict owner-occupation rules

Restricted. Approval rarely granted.

- All other landed property in Singapore (bungalows, semi-detached, terrace houses)

Closed to foreigners.

- HDB resale flats (with very narrow PR exceptions, not foreigner exceptions)

- BTO flats

- New ECs in their first 10 years

The landed-property catch

Landed property is the dream for most high-net-worth buyers moving to Singapore. The reality is harder. To buy a landed home outside Sentosa Cove, a foreigner needs approval from the Land Dealings Approval Unit (LDAU) under the Singapore Land Authority. The criteria are tight:

- Permanent Resident status for at least 5 years

- Significant economic contribution to Singapore, judged on taxable employment income and business presence

- A satisfactory record (no bankruptcy, no criminal record)

Approval rates are low. Most successful applicants are PRs who have lived in Singapore for over a decade, run businesses here, and pay substantial Singapore tax. Even then, the process takes 12 to 16 weeks and a refusal carries no appeal.

Sentosa Cove is the workaround. It is the only place in Singapore where a foreigner can buy a landed home without LDAU approval. Two conditions apply. The property must be used for owner-occupation only, with no rental allowed at any term. And the land area is capped at 1,800 square metres. Prices on Sentosa Cove start around $5 million and run past $15 million for waterfront bungalows.

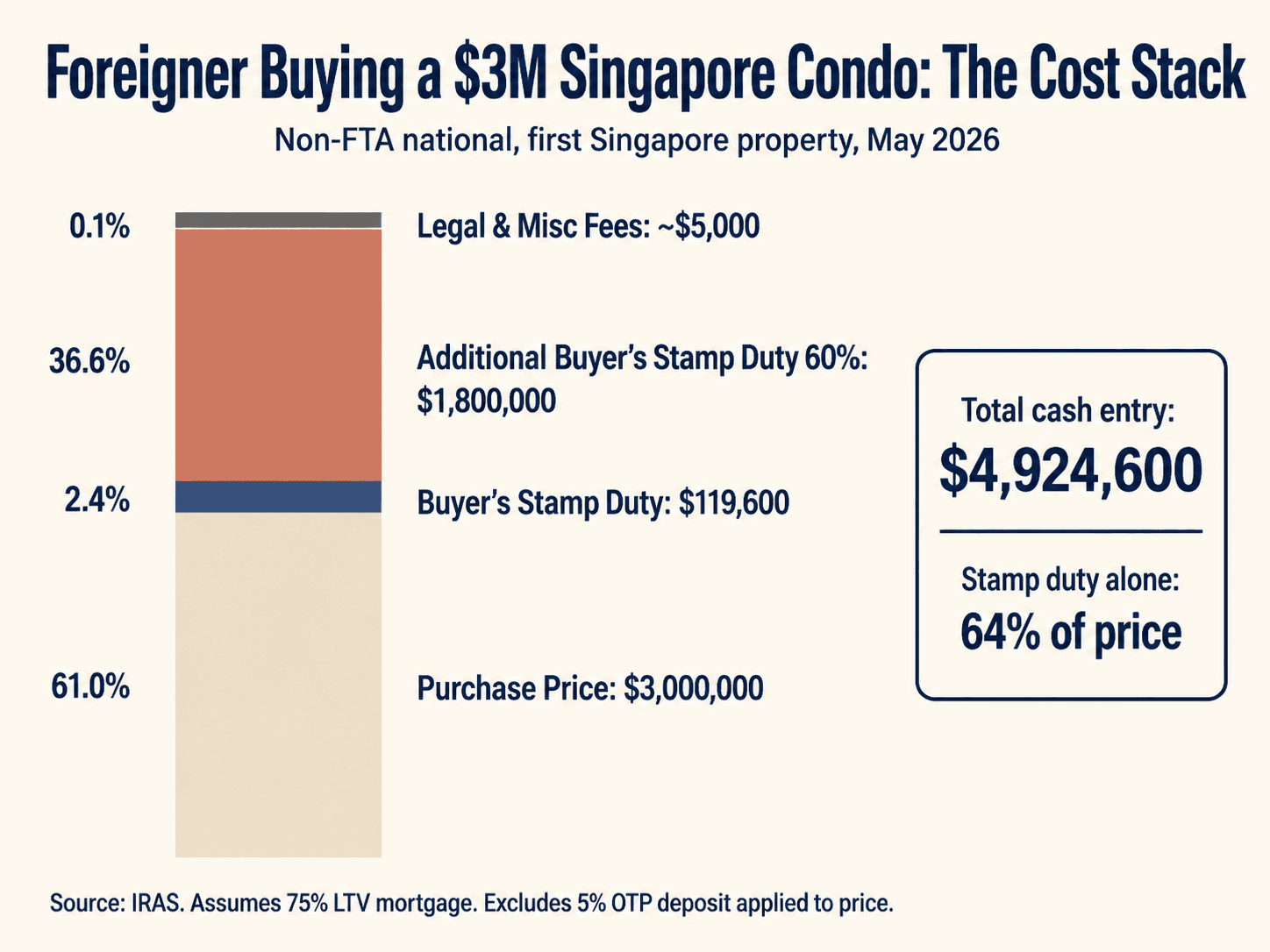

The cost stack

For a non-FTA foreigner buying a $3 million private condo as a first Singapore property, the breakdown looks like this:

| Cost | Amount | % of price |

|---|---|---|

| Purchase price | $3,000,000 | 100% |

| Buyer's Stamp Duty (BSD) | $119,600 | 4.0% |

| Additional Buyer's Stamp Duty (ABSD) at 60% | $1,800,000 | 60% |

| Legal fees (conveyancing) | $3,000 to $5,000 | 0.2% |

| Property valuation | $300 to $700 | < 0.1% |

| Mortgage stamp duty | up to $500 | < 0.1% |

| Total outlay, price plus all duties and fees, paid fully in cash | ~$4,923,000 | ~164% |

That total assumes the full price is paid in cash. With financing of up to 75% on a first property, the cash you actually need is lower, though every duty and fee above is payable in cash regardless. The 60% ABSD line is what kills most deals. Total stamp duty alone is 64% of the purchase price. For a non-resident with no FTA exemption, the numbers rarely work below the $5 million mark, because the stamp duty adds so much to the entry cost.

Who qualifies for the FTA exemption

Five nationalities receive what IRAS calls "national treatment" under Singapore's Free Trade Agreements. They pay the same stamp duty rates as a Singapore Citizen on their first residential property, which means 0% ABSD.

- United States. Citizens only. Green card holders do not qualify.

- Iceland. Nationals and permanent residents.

- Liechtenstein. Nationals and permanent residents.

- Norway. Nationals and permanent residents.

- Switzerland. Nationals and permanent residents.

For a US citizen buying the same $3 million condo, the ABSD line drops from $1.8 million to zero. Total stamp duty becomes $119,600 instead of $1,919,600.

The exemption only applies to the first residential property. A US citizen buying a second Singapore property pays the foreigner rate of 60% on that one. There is no FTA route around it. For a full breakdown of the rates and remission process, see our complete 2026 ABSD guide.

Whether you qualify for the FTA exemption can change your stamp duty by hundreds of thousands of dollars. Message me to check your FTA eligibility.

Financing as a non-resident

Three numbers drive everything.

Loan-to-Value cap (LTV). A foreigner with a clean record can borrow up to 75% of the property value on their first private residential property, provided the loan tenure is 30 years or less and ends before age 65. For a second property, LTV drops to 45%. For a third, 35%. The remainder must be paid in cash.

Total Debt Servicing Ratio (TDSR). All monthly debt obligations cannot exceed 55% of gross monthly income, stress-tested at a 4% interest rate. This is enforced by every Singapore-licensed bank, no exceptions. It captures the new mortgage, any car loans, credit card minimums, and existing property loans abroad.

Loan tenure cap. 30 years maximum for private residential. Beyond age 65 or above 75% LTV, banks tighten further.

Most foreigners go through the local big three. DBS, OCBC, and UOB hold around 80% of the Singapore mortgage market between them. They process IPAs (In-Principle Approval) within 5 to 10 business days for straightforward employment-pass applicants. If your income is harder to document, for example from offshore trusts, payroll across several countries, or a business that retains its earnings, then HSBC, Standard Chartered, and Maybank tend to be more flexible. Most foreign-bank private banking arms require a minimum loan size of $500,000.

Documents to prepare for the IPA:

- Passport

- Employment Pass, S-Pass, or Dependant's Pass

- Last 6 months of payslips

- Latest tax filing or Notice of Assessment

- 3 to 6 months of bank statements

- Existing loan statements if applicable

The actual buying timeline

For a non-resident buyer who is not physically in Singapore, the full sequence takes 8 to 12 weeks from search to keys. The compressed version:

Week 1 to 4. Search and IPA. Shortlist properties with a licensed agent. Apply to two banks for IPA in parallel. The bank with the better rate gets the financing job. IPAs are valid for 30 days, sometimes 60.

Week 4 to 5. OTP exercise. Pay the 5% Option to Purchase fee. From the OTP date you have 14 calendar days to exercise (sign) the option. This is when your conveyancing lawyer earns their fee. They will check the Sale & Purchase Agreement, title, encumbrances, and lease balance.

Week 5 to 6. Stamping and ABSD. BSD and ABSD must be paid within 14 days of the contract date. Pay through IRAS e-Stamping. FTA-exempt buyers apply for remission within the same 14-day window via myTax Portal. The exemption usually clears in 2 to 4 weeks.

Week 6 to 12. Completion. For a resale, completion runs 8 to 12 weeks after OTP. The balance 20% of the purchase price (less the 5% OTP already paid, plus the 75% loan) plus all legal costs settle on completion day. Keys are handed over. For a new launch, you pay via the Progressive Payment Scheme over the build period, typically 3 to 4 years, with the balance at Temporary Occupation Permit.

Remote buyers can sign almost everything digitally. SingPass is required for myTax Portal access. Non-residents without SingPass can authorise a Singapore-based representative through a Power of Attorney to handle stamping and completion.

Where foreigners actually buy

The market data is clear on this. Non-resident buyers concentrate in five postcodes:

- District 9. Orchard, River Valley, Killiney. The default for first-time foreign buyers. Walking distance to everything, deep resale market, predictable price floors. Browse District 9 listings.

- District 10. Bukit Timah, Holland, Tanglin. The HNW corridor. Schools matter here (NJC, ACS, Hwa Chong) and proximity to them prices in. Browse District 10 listings.

- District 11. Novena, Newton, Thomson. Quieter than D9, slightly cheaper, strong medical-precinct demand.

- District 1 and District 2. CBD, Marina Bay, Tanjong Pagar. Vertical living, strong rental yields, the choice for younger expats and those running businesses in Raffles Place.

- Sentosa Cove. The landed exception, owner-occupiers only.

Foreigners buy far less in the heartland districts (D14, D15, D16, D19) because the rental demand from other foreigners is weaker outside the central belt. The price discount versus central is real but the resale liquidity is thinner.

Bottom line

Singapore property is open to foreigners on paper, expensive in practice, and gated on the landed side. The condominium market is the practical entry point for anyone without an FTA exemption, and the tax stack means most non-resident buyers transact above $2 million if they buy at all.

Three things to plan around. First, decide if you qualify for the FTA exemption before you start looking. Second, get an IPA from two banks early. Third, never quote yourself the headline price. Quote yourself headline plus BSD plus ABSD. That is the real entry cost.

I can confirm what you can buy, your true cost stack, and your financing options before you fly in. Get a foreigner-buyer consult on WhatsApp.

Further reading

- ABSD Singapore Explained: Rates, Remission, and the Full 2026 Breakdown. The full rates matrix, remission flow, and worked examples.

- District 10 Singapore: A Property Guide to Bukit Timah, Holland, and Tanglin. Where the highest-volume foreign-buyer activity sits.

- Singapore Cooling Measures: The Full History and What's Likely in 2026. Why ABSD is what it is, and what could move next.

Sources

- IRAS — Additional Buyer's Stamp Duty (ABSD)

- IRAS — Buyer's Stamp Duty (BSD)

- IRAS — ABSD Remission under Free Trade Agreements

- Singapore Land Authority — Foreign Ownership of Property

- Residential Property Act 1976 — Singapore Statutes Online

- MAS — Total Debt Servicing Ratio

Common questions about foreigners buying Singapore property

Can a foreigner buy property in Singapore?

Yes. Foreigners can buy private condominiums, apartments, strata units in approved developments, fully privatised Executive Condominiums over ten years old, and commercial property without approval. Landed homes outside Sentosa Cove need Land Dealings Approval Unit clearance, which is rarely granted. HDB flats are closed to foreigners.

How much stamp duty does a foreigner pay on a Singapore condo?

A foreigner pays 60% ABSD plus Buyer's Stamp Duty of up to 6%. On a $3 million condo that is about $1.92 million in stamp duty before keys change hands. Nationals of the United States, Iceland, Liechtenstein, Norway, and Switzerland pay 0% ABSD on a first property under Free Trade Agreements.

Can a foreigner get a home loan in Singapore?

Yes. A foreigner with a clean record can borrow up to 75% of the property value on a first private home, subject to a Total Debt Servicing Ratio of 55% of gross monthly income, stress-tested at 4%. The local banks DBS, OCBC, and UOB hold most of the market, while HSBC, Standard Chartered, and Maybank tend to be more flexible on complex income.

How long does it take a foreigner to buy a Singapore property?

About eight to twelve weeks from search to keys for a resale. The sequence runs through in-principle loan approval, the Option to Purchase, exercising the option, stamping within 14 days, and completion. Remote buyers can sign most documents digitally or appoint a Singapore representative through a Power of Attorney.

This article is for general information only and should not be considered financial, legal, tax, or investment advice. Property decisions should be based on individual circumstances and independent professional advice.

About the Author

Winnie Lim is a licensed CEA real estate agent and the founder of AIProperty.sg. With a background in supply chain analytics, she brings a data-driven approach to Singapore property, and won the 2024 Million Dollar Award for consistent, client-first results.

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Licence L3008899K)

Read full bio →Continue Reading

More from Buying Guide

How Much Do You Really Need to Buy a Condo in Singapore? Down Payment, TDSR and Stamp Duty

How much cash and CPF you really need to buy a condo in Singapore in 2026: the 25% down payment and 5% cash rule, the TDSR loan limit, Buyer's Stamp Duty, and the full upfront cost on a $2 million example.

01 Jul 2026

How HDB Upgraders Avoid ABSD in 2026: Sell-First vs Decoupling

How Singapore HDB upgraders legally avoid or recover ABSD in 2026: the sell-first route, the buy-first 6-month remission, why you cannot decouple an HDB, and how decoupling works for private owners.

30 Jun 2026

The Crab Bucket Effects

Crab Mentality Part 1 - Buyers (Are you one of them?)

08 Jun 2026