Singapore Cooling Measures: The Full History and What's Likely in 2026

15 May 2026 · 8 min read

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Estate Agent Licence L3008899K) · Updated 24 June 2026

“Data-driven property advice. Straight talk, no hype.”

Singapore Cooling Measures: The Full History and What's Likely in 2026

Singapore has run more property-cooling rounds than any other major market in Asia. Fifteen rounds since 2009. New tools added, old tools tightened, rates revised whenever transaction data starts running hot. The combined effect is a property market whose growth is held back by taxes and lending limits rather than set purely by supply and demand.

This guide walks through every round from 2009 to 2025, explains what each tool actually does, and outlines what is still in force in 2026. Numbers are pulled from IRAS, MAS, HDB, and the Ministry of National Development.

Why cooling measures exist

The reason is buried in 2008. After the global financial crisis, Singapore property prices started running again on a wave of cheap money and foreign capital. The Government's concern was not just price inflation. It was structural: a property bubble in Singapore would damage household balance sheets, drive up household debt, and price citizens out of their own housing market. Cooling measures are the policy instrument that prevents that.

Three goals run through every round.

- Slow speculation. Discourage flip transactions and short-hold investment by taxing exit.

- Protect Singapore Citizens. Keep the demand stack tilted toward owner-occupier locals, not foreign capital or local investors.

- Restrain household leverage. Cap loan-to-value, cap debt-servicing-ratio, prevent over-borrowing at the macro level.

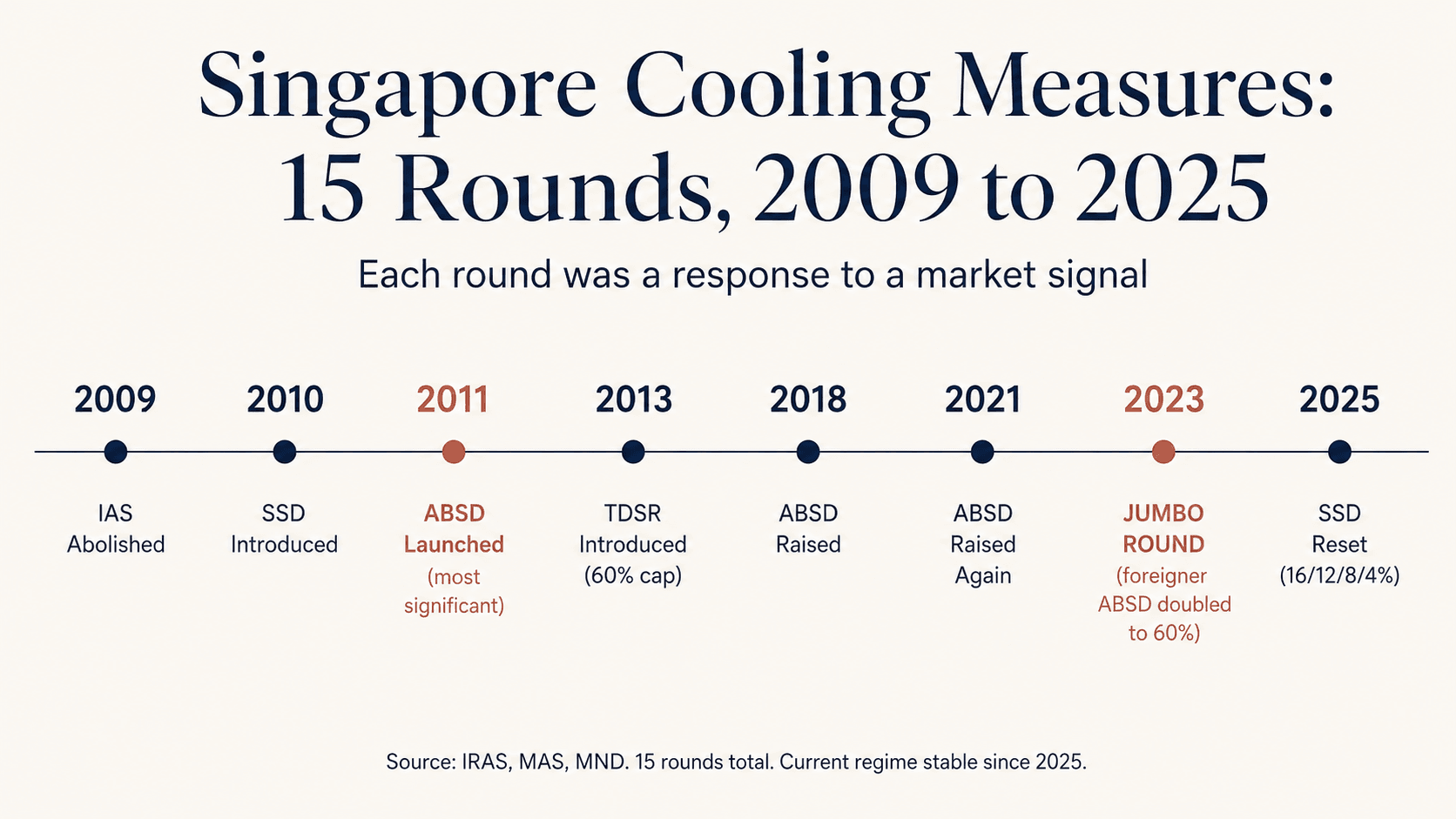

The full timeline: 2009 to 2025

| Year | Round | Headline change |

|---|---|---|

| Sep 2009 | 1 | Interest Absorption Scheme abolished. Developers can no longer pre-fund deferred-payment buyers. |

| Feb 2010 | 2 | Seller's Stamp Duty (SSD) introduced for properties sold within one year. LTV cap lowered to 80%. |

| Aug 2010 | 3 | SSD extended to a three-year holding period. LTV reduced for second-property loans. |

| Jan 2011 | 4 | SSD rates raised (16%, 12%, 8%, 4% over four years). LTV cut further. |

| Dec 2011 | 5 | Additional Buyer's Stamp Duty (ABSD) introduced. 10% on foreigners, 3% on PRs (2nd+), 3% on SC (3rd+). |

| Oct 2012 | 6 | Maximum loan tenure capped at 35 years. |

| Jan 2013 | 7 | ABSD rates raised significantly. Tighter cash down-payment for second loans. |

| Jun 2013 | 8 | Total Debt Servicing Ratio (TDSR) introduced at 60%. Stress-tested at 3.5% then later 4%. |

| Mar 2017 | 9 | SSD partially relaxed (holding period cut from 4 to 3 years, rates lowered). |

| Jul 2018 | 10 | ABSD raised again. Foreigners to 20%. SC 2nd from 7% to 12%. LTV tightened. |

| Dec 2021 | 11 | ABSD raised again. SC 2nd to 17%. Foreigners to 30%. HDB loan TDSR floor rate raised. |

| Sep 2022 | 12 | HDB LTV cut to 80%. 15-month wait-out introduced for private property owners buying HDB resale. TDSR/MSR floor rates raised. |

| Apr 2023 | 13 | The jumbo round. Foreigner ABSD doubled from 30% to 60%. Entity ABSD raised from 35% to 65%. SC 2nd from 17% to 20%. SC 3rd from 25% to 30%. |

| Aug 2024 | 14 | HDB LTV further reduced to 75%. |

| Jul 2025 | 15 | SSD reverted to pre-2017 framework. Four-year holding period restored. Rates raised by 4 percentage points at each tier (16%/12%/8%/4%). |

The 2023 jumbo round

The April 2023 round is the most significant of the past decade. Foreigners went from 30% ABSD to 60% overnight, with no transition period for buyers mid-transaction. The market reaction was immediate. New launch sales the following month halved versus the prior month. Foreign-buyer transaction share dropped from 7.4% of private home sales in Q1 2023 to under 2% by year-end.

The policy logic was political as much as macroeconomic. Foreign demand had concentrated in District 9, District 10, and District 11 prime stock, pushing prices into ranges that locked out younger Singaporean buyers even with full leverage. The 60% ABSD effectively priced foreigners out of the bottom half of the market and pushed the remaining foreign buyers to high-ticket trophy purchases above $5 million, which is exactly where the Government wanted them.

For the full mechanics of ABSD as it stands in 2026, see our complete ABSD guide.

What each tool actually does

ABSD (Additional Buyer's Stamp Duty) is a transaction tax on the buyer side, charged on top of normal BSD. Rates depend on residency status and the number of properties owned. Foreigners hit 60%, entities 65%, citizens 0% on first and 20-30% on additional. ABSD discourages multi-property hoarding and foreign investment.

SSD (Seller's Stamp Duty) is a transaction tax on the seller side, charged on properties sold within a defined holding period. As of July 2025, the rates are 16% (Year 1), 12% (Year 2), 8% (Year 3), 4% (Year 4). Sell after Year 4 and SSD is zero. SSD discourages flipping and short-hold speculation.

LTV (Loan-to-Value cap) sets the maximum percentage of property price that can be financed by a mortgage. Singapore residents and PRs get up to 75% on a first private property. HDB buyers using the HDB loan get up to 75% (post-August 2024 cut). Second-property LTV drops to 45%. Third drops to 35%. The rest must be in cash and CPF.

TDSR (Total Debt Servicing Ratio) caps a borrower's monthly debt obligations at 55% of gross monthly income, stress-tested at a 4% interest rate. It captures all debts, not just the new mortgage. Car loans, credit card minimums, study loans, and existing property loans all count.

MSR (Mortgage Servicing Ratio) is HDB-specific. It caps the mortgage payment (only) at 30% of gross monthly income, stress-tested at 4%. It applies on top of TDSR for HDB loans. The tighter of the two binds.

Loan tenure cap. Private property loans are capped at 30 years. HDB loans at 25 years. Beyond age 65 or above 75% LTV, banks tighten further.

Each tool, ABSD, LTV, and TDSR, hits buyers and sellers differently depending on where you stand. Message me to map your position.

Did they work?

Mixed but mostly yes, on the metric that matters most.

The Private Property Price Index, after running at 8-15% annual growth in 2011-2013, has averaged around 2-4% annual growth in the post-jumbo regime (April 2023 onwards). That is closer to wage growth than to historical Singapore property cycles.

Foreign demand collapsed exactly as designed. The foreign share of private residential transactions averaged 7-9% in the 2018-2022 window. It is under 2% in 2025-2026.

Speculative volume is also down. Sub-sale transactions, where a buyer resells an uncompleted unit before TOP, ran at roughly 5% of new-sale volume before 2017. The July 2025 SSD reset cut sub-sales by an estimated 60% in the first quarter under the new rules.

The downside is that the cooling stack adds friction for legitimate transactions. Upgraders now face a 6-month ABSD remission window that often forces bridge financing. Foreign buyers with FTA exemptions navigate three sets of forms before stamping. The system protects citizens but slows the market for everyone.

What's likely next in 2026

The current government position is "watch and adjust." Cooling measures are not reversed unless the market clearly under-shoots, and Singapore property in 2026 is growing within target. So nothing is imminent.

That said, three areas are worth watching.

ABSD recalibration on foreigners. The 60% rate is the highest in the developed world, and there is industry lobbying for a modest cut, possibly to 40-45%, paired with stricter eligibility (longer Singapore tax residency requirements). Probability in 2026: low to moderate. The Government has shown no urgency.

HDB loan tightening on PRs. PR demand for HDB resale has been steady despite the 2022 wait-out rule for private downgraders. If PR demand continues squeezing local buyers in popular estates, expect MSR or LTV cuts targeting PRs specifically. Probability: moderate.

SSD extension to commercial. Commercial real estate currently has no SSD. If the speculative pressure pushed out of residential lands in commercial (and it partially has), expect a commercial SSD parallel to the residential rules. Probability: low in 2026, rising into 2027.

What is not on the table. ABSD cuts for citizens. HDB MOP relaxation. TDSR cap raise. These are pillars of the regime, not levers.

Bottom line

Singapore's cooling measures are not a single policy. They are a layered, 15-round system built over 16 years, with each round closing a loophole or responding to a specific market signal. The current 2026 stack is stable, well-tested, and designed to keep growth modest and citizens housed.

If you are buying, plan your transaction around the stack rather than against it. Know the ABSD remission rules. Know the SSD holding period before you sell. Know your TDSR and MSR before you finalise the loan. The cooling measures will not loosen for you, but they are predictable. That predictability is the whole point.

I can show you exactly which cooling measures touch your purchase or sale, and how to time it. Get a no-obligation plan on WhatsApp.

Further reading

- ABSD Singapore Explained: Rates, Remission, and the Full 2026 Breakdown. The biggest single tool in the cooling stack, broken down.

- Buying Property in Singapore as a Foreigner: The Complete 2026 Guide. How the 2023 jumbo round changed the foreigner playbook.

- How to Sell Your HDB Flat in Singapore. The MOP, ABSD upgrader trap, and 15-month wait-out rule in practice.

Sources

- IRAS — Additional Buyer's Stamp Duty (ABSD)

- IRAS — Seller's Stamp Duty (SSD)

- MAS — Total Debt Servicing Ratio (Notice 645A)

- MAS — Cooling Measures Press Releases

- Ministry of National Development — Cooling Measures Announcements

- HDB — Loan-to-Value and Eligibility

Common questions about Singapore cooling measures

What are property cooling measures in Singapore?

They are government tools that slow speculation, protect Singapore Citizens, and limit household borrowing. The main ones are ABSD, Seller's Stamp Duty, the Loan-to-Value cap, the Total Debt Servicing Ratio, and the Mortgage Servicing Ratio. Singapore has run fifteen rounds since 2009.

What was the 2023 cooling measure?

In April 2023, foreigner ABSD doubled from 30% to 60% and entity ABSD rose to 65%, with no transition period. New launch sales the following month halved, and the foreign-buyer share fell from 7.4% of private home sales to under 2% by year-end. This is the most significant round of the past decade.

Are Singapore cooling measures likely to ease in 2026?

Not imminently. The government's position is to watch and adjust, and prices are growing within target at about 2 to 4% a year. Industry has lobbied for a modest foreigner ABSD cut, but no change has been signalled.

What is the difference between TDSR and MSR?

TDSR caps all monthly debt at 55% of gross monthly income and applies to every property loan. MSR is HDB-specific and caps only the mortgage payment at 30% of gross monthly income. Both are stress-tested at 4%, and for HDB loans the tighter of the two applies.

This article is for general information only and should not be considered financial, legal, tax, or investment advice. Property decisions should be based on individual circumstances and independent professional advice.

About the Author

Winnie Lim is a licensed CEA real estate agent and the founder of AIProperty.sg. With a background in supply chain analytics, she brings a data-driven approach to Singapore property, and won the 2024 Million Dollar Award for consistent, client-first results.

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Licence L3008899K)

Read full bio →Continue Reading

More from Market Trends

Lentor Modern Resale Analysis: Are Early Buyers Winning?

Lentor Modern resale data shows early buyers profiting up to $590,000 on larger units and about $150,000 on 732 sqft two bedroom units after three years.

25 May 2026

Senja Million Dollar HDBs

The rise of Senja's million-dollar HDB flats has owners asking if now is the time to upgrade to an Executive Condominium.

19 May 2026

EC Cooling Measures 2026

Major changes announced for Executive Condominiums (ECs) in Singapore 🇸🇬

15 May 2026