ABSD Singapore Explained: Rates, Remission, and the Full 2026 Breakdown

15 May 2026 · 10 min read

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Estate Agent Licence L3008899K) · Updated 24 June 2026

“Data-driven property advice. Straight talk, no hype.”

ABSD Singapore Explained: Rates, Remission, and the Full 2026 Breakdown

If you are buying property in Singapore this year, ABSD is the line item that will hurt the most. Buyer's Stamp Duty caps out at 6%. The Additional Buyer's Stamp Duty can hit 60% before you have signed anything.

That is not a typo. A foreign buyer purchasing a $3 million condo in District 9 pays $1.8 million in ABSD on top of the price. Then BSD on top of that. The math gets brutal fast.

This guide covers the current rates, who pays what, how the remissions work, and the legitimate ways married couples and FTA nationals reduce the bill. Numbers are accurate to May 2026 and verified against the official IRAS ABSD page. The rates have held since 27 April 2023 and no changes were announced in Budget 2026.

What ABSD is, and why it exists

ABSD was introduced in December 2011 as a cooling measure. The Government wanted to slow speculation, prevent overheating, and keep Singapore Citizens from being priced out of the housing market by foreign capital and investor demand.

It is not a tax on owning property. It is a one-shot tax paid within 14 days of the contract date, calculated on the higher of purchase price or market value. Miss the 14-day window and you incur a penalty of up to four times the duty owed.

The rates have been raised five times since 2011. The biggest jump came on 27 April 2023, when foreigners went from 30% to 60% and Singapore Citizens buying a second property went from 17% to 20%. That round caught the market off guard. New launches in the weeks that followed saw transaction volumes halve overnight.

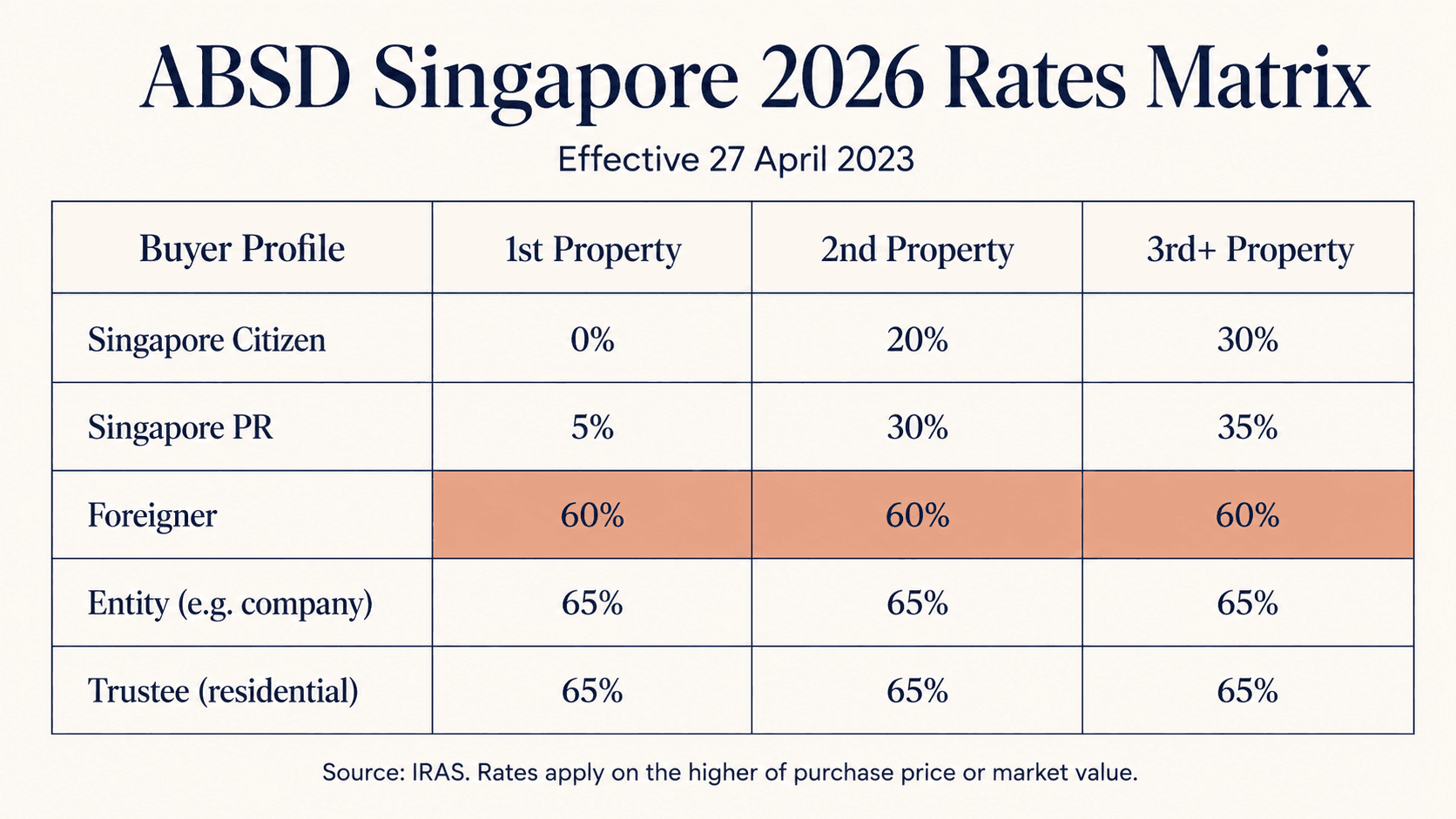

The 2026 ABSD rates

These are the rates as of May 2026, unchanged since April 2023:

| Buyer profile | 1st property | 2nd property | 3rd+ property |

|---|---|---|---|

| Singapore Citizen | 0% | 20% | 30% |

| Singapore PR | 5% | 30% | 35% |

| Foreigner | 60% | 60% | 60% |

| Entity (e.g. company) | 65% | 65% | 65% |

| Trustee (residential) | 65% | 65% | 65% |

Foreigners pay 60% regardless of whether it is their first, fifth, or fifteenth Singapore property. PRs pay 5% on their first one. Citizens pay nothing on the first.

ABSD is computed on the higher of purchase price or market value. If you buy a $1.5M condo and the IRAS valuer pegs market at $1.6M, ABSD is calculated on $1.6M.

How BSD stacks on top

Every buyer pays Buyer's Stamp Duty in addition to ABSD. The BSD scale is progressive:

| Slice of price | BSD rate |

|---|---|

| First $180,000 | 1% |

| Next $180,000 | 2% |

| Next $640,000 (up to $1M) | 3% |

| Next $500,000 (up to $1.5M) | 4% |

| Next $1.5M (up to $3M) | 5% |

| Anything above $3M | 6% |

On a $2 million purchase, BSD works out to $69,600. On a $3 million purchase, it is $119,600. Both rates have held since 15 February 2023.

Worked examples

Example 1: Singapore Citizen, first private property at $2M

- BSD: $69,600

- ABSD: $0

- Total stamp duty: $69,600 (3.5% of price)

This is the cleanest scenario. A first-timer Singaporean buying a private condo pays only the progressive BSD. Cash up front within 14 days of OTP exercise.

Example 2: Singapore Citizen couple upgrading to a $2M condo, still holding their HDB

- BSD: $69,600

- ABSD: 20% of $2M = $400,000

- Total stamp duty at purchase: $469,600

The 20% ABSD hits because they technically own two properties at the point of purchase. They can claim a refund if they sell their HDB within 6 months of the OTP date for the new condo, or within 6 months of TOP if buying a new launch. Application for refund must be made within 6 months after the HDB sale completes.

This is the most common ABSD pain point in the upgrader market. Sellers usually need bridging finance for the gap.

Example 3: Foreign buyer (non-FTA national) at a $3M condo

- BSD: $119,600

- ABSD: 60% of $3M = $1,800,000

- Total stamp duty: $1,919,600 (64% of the purchase price, in additional cash)

This is what stops most foreigners from buying. A Chinese, Indonesian, or Australian buyer at this price level needs almost two million dollars in cash on top of the purchase price, the legal fees, and the deposit. ABSD alone equals roughly two decades of likely prime-district rental income.

Example 4: US national at the same $3M condo

- BSD: $119,600

- ABSD: $0 (first property, FTA national treatment)

- Total stamp duty: $119,600

US citizens get treated as Singapore Citizens for stamp duty purposes under the US-Singapore Free Trade Agreement. The same national treatment applies to nationals and permanent residents of Iceland, Liechtenstein, Norway, and Switzerland under the European Free Trade Association FTA. They pay the Singapore Citizen ABSD rate at every property they buy — 0% on the first, 20% on the second, 30% on a third or more — rather than the 60% foreigner rate. The biggest win is on the first property, where the SC rate is 0%.

For Americans, this is a meaningful arbitrage. Green card holders do not qualify. Only US passport holders do.

Citizen, PR, foreigner, or married couple, each sits on a different rate and a different remission path. Message me for a personalised ABSD and stamp-duty breakdown.

ABSD remission for married couples

This is the most-used path for upgraders. The conditions are tight:

- Both spouses must purchase the second property in joint names only. No siblings, parents, children on title.

- At least one spouse must be a Singapore Citizen.

- Neither spouse can own any other residential property at the time the refund is claimed.

- The first property must be sold within 6 months of the second purchase, or within 6 months of TOP/CSC for new launches, whichever applies.

Miss any one of these and the ABSD becomes permanent. The application is filed through myTax Portal within 6 months of the first property sale completing.

A common mistake. Couples buy in only one spouse's name to "preserve" the other's first-timer status. This works only if the buying spouse genuinely has no interest in the first property. If both names are on the existing title, the remission later cannot apply.

ABSD remission under Free Trade Agreements

Five nationalities qualify under FTAs:

- United States. Citizens only, not green card holders.

- Iceland. Nationals and permanent residents.

- Liechtenstein. Nationals and permanent residents.

- Norway. Nationals and permanent residents.

- Switzerland. Nationals and permanent residents.

Eligible buyers receive what IRAS calls "national treatment." This means they pay the same stamp duty rates as a Singapore Citizen at every stage of property ownership, so 0% ABSD on a first property instead of the 60% foreigner rate. A first-time US-citizen buyer pays 0% ABSD and the standard BSD on top.

The exemption is claimed by submitting an application via myTax Portal within 14 days of stamping. IRAS typically reviews within 2 to 4 weeks. If approved at the point of stamping, ABSD is not paid in the first place. If paid first then claimed, the refund is processed back later.

Under national treatment, an FTA national buying a second Singapore property pays 20% ABSD (the Singapore Citizen rate), not the 60% foreigner rate. A third or subsequent property is taxed at 30% (again, the SC rate). The 60% foreigner rate never applies to qualifying FTA nationals — that is the entire point of national treatment.

Decoupling: legitimate, but watched

Decoupling is the formal name for one co-owner selling their share to the other so that the exiting party becomes a first-timer for their next purchase. For private property, it is legal and reasonably common.

Typical cost of decoupling a $1.5M freehold or leasehold private condo:

- Legal fees: $3,000 to $5,000

- Valuation: $500 to $1,500

- Bank mortgage discharge and reapplication: $2,000 plus 0.5 to 1% loan processing

- BSD on the transferred share (the spouse "buying out" the other half pays BSD on that half)

- Possible SSD if the property is under 3 years from original purchase

A clean decoupling on a $1.5M condo usually runs around $40,000 to $50,000 all-in. Versus 20% ABSD on a second $1.5M property ($300,000), the math is obvious.

Two things to know.

HDB flats cannot be decoupled. The only exception is a court-ordered transfer in divorce proceedings.

99-to-1 schemes are now penalised. In May 2024, IRAS clawed back roughly $60 million in stamp duties from buyers who had structured ownership as 99% to one spouse and 1% to the other, then later "decoupled" the 1% to manufacture a first-timer. The clawback includes the original ABSD plus a 50% surcharge plus interest. On a $300,000 ABSD case, that becomes $450,000 plus interest and legal fees. Do not go near it.

How to plan around ABSD without breaking anything

Three patterns the upgrader market actually uses:

- Sell first, buy second. Move into a short-term rental for 6 to 12 months. Buy the next property as a first-timer with no ABSD exposure. Slowest path, but the cleanest.

- Buy in one spouse's name only. Works if that spouse genuinely owns nothing else. Marriage does not automatically make spouses joint owners. But if the first property is already in both names, this route is closed.

- Pay ABSD upfront and claim the refund on time. This is the most common path. The buyer needs the cash up front, sometimes $300,000 to $500,000, then waits up to 6 months for the refund. Bridge loans are available. Cost is roughly 4 to 6% per annum on the bridged amount.

For foreigners, the planning looks different. If you do not qualify under an FTA, your options narrow:

- Apply for Singapore PR before buying. PR rates start at 5% on the first property, still a meaningful saving on 60%.

- Wait for a project where the developer absorbs ABSD through a rebate. These are rare, usually on slow-selling tail units. The new launches under S$3 million are where most rebate activity surfaces.

- Buy commercial property instead. ABSD does not apply to commercial real estate.

When ABSD does not apply

A short list of property types and structures that fall outside the ABSD regime:

- Commercial property (offices, retail, industrial)

- Mixed-use developments where the residential portion is below the size IRAS uses to apply ABSD

- Inheritance, since it is not a "purchase" and does not trigger ABSD

- Gifts between family members where no consideration changes hands (BSD may still apply on the market value)

Property bought under a company structure still incurs the 65% entity ABSD, so the "buy through a shell company" route does not work.

Bottom line

ABSD is the single largest tax decision in any Singapore property purchase. For a Singapore Citizen first-timer, it is nothing. For a foreigner, it is the deal-killer for the bottom half of the market.

The remissions work, but only if the conditions are met exactly. The FTA exemption is the strongest tool for those who qualify. The married-couple remission catches most upgraders if they plan around the 6-month window. Decoupling is legal but the 99-to-1 era is over.

If you are sizing a budget for Singapore property, do not quote yourself the headline price. Quote yourself headline plus BSD plus ABSD. That is the real entry cost.

I can map your exact stamp-duty cost and any remission you qualify for before you sign anything. Get your ABSD timing plan on WhatsApp.

Further reading

- Buying Property in Singapore as a Foreigner: The Complete 2026 Guide. Full breakdown of eligibility, financing, and timeline for non-resident buyers.

- Singapore Cooling Measures: The Full History and What's Likely in 2026. Every cooling measure round from 2009 onwards, and what each one was designed to fix.

- Browse District 9 listings and District 10 listings. The two districts where most ABSD-paying foreign buyers transact.

Sources

- IRAS — Additional Buyer's Stamp Duty (ABSD)

- IRAS — Buyer's Stamp Duty (BSD)

- IRAS — ABSD Remission for Married Couples

- IRAS — ABSD Remission under Free Trade Agreements

- MOF — Tax Concessions under Free Trade Agreements

- Stamp Duties (Spouses) (Remission of ABSD) Rules 2013

Common questions about ABSD in Singapore

How much ABSD does a foreigner pay in Singapore in 2026?

A foreigner pays 60% ABSD on every residential property purchase, regardless of whether it is their first or fifth. This rate has held since 27 April 2023. Nationals of the United States, Iceland, Liechtenstein, Norway, and Switzerland are treated as Singapore Citizens under Free Trade Agreements and pay 0% on a first property.

Can married couples get their ABSD refunded?

Yes, if at least one spouse is a Singapore Citizen, the new property is bought in joint names, and the first property is sold within 6 months of the purchase, or within 6 months of TOP for a new launch. The refund is claimed through myTax Portal. Miss any condition and the ABSD becomes permanent.

When is ABSD payable after signing?

ABSD is due within 14 days of the contract date, calculated on the higher of purchase price or market value. Paying late incurs a penalty of up to four times the duty owed. It is a one-time tax, not an annual charge.

Does buying through a company avoid ABSD?

No. A residential purchase under a company or entity structure attracts 65% ABSD, higher than the 60% foreigner rate. Decoupling is legal for private property, but HDB flats cannot be decoupled outside a court-ordered divorce transfer.

This article is for general information only and should not be considered financial, legal, tax, or investment advice. Property decisions should be based on individual circumstances and independent professional advice.

About the Author

Winnie Lim is a licensed CEA real estate agent and the founder of AIProperty.sg. With a background in supply chain analytics, she brings a data-driven approach to Singapore property, and won the 2024 Million Dollar Award for consistent, client-first results.

CEA Salesperson Registration: R061623D · Huttons Asia Pte. Ltd (Licence L3008899K)

Read full bio →Continue Reading

More from Investment & Finance

Freehold vs Leasehold (D11 Newton)

A new Newton GLS site sold above Pullman Residences' freehold land cost. We compare freehold vs leasehold and what it means for D11 prices.

10 Jun 2026

Is a $3.58 million loss really a loss? A deep dive into Marina Bay Residences

Marina Bay Residences penthouse sold at a $3.58 million paper loss. After 19 years of rental income, was it really a loss? We run the numbers.

28 May 2026

Dairy Farm Land Price Analysis

A look at how Dairy Farm land prices have risen over the years, and whether buying into the area today is still a good move.

22 May 2026